Welcome to DU!

The truly grassroots left-of-center political community where regular people, not algorithms, drive the discussions and set the standards.

Join the community:

Create a free account

Support DU (and get rid of ads!):

Become a Star Member

Latest Breaking News

Editorials & Other Articles

General Discussion

The DU Lounge

All Forums

Issue Forums

Culture Forums

Alliance Forums

Region Forums

Support Forums

Help & Search

Environment & Energy

Related: About this forumIEA: Global Energy Review 2026 - CO2 emissions

(Please note: The following content is taken from a Creative Commons source.)

IEA (2026), Global Energy Review 2026, IEA, Paris https://www.iea.org/reports/global-energy-review-2026, Licence: CC BY 4.0

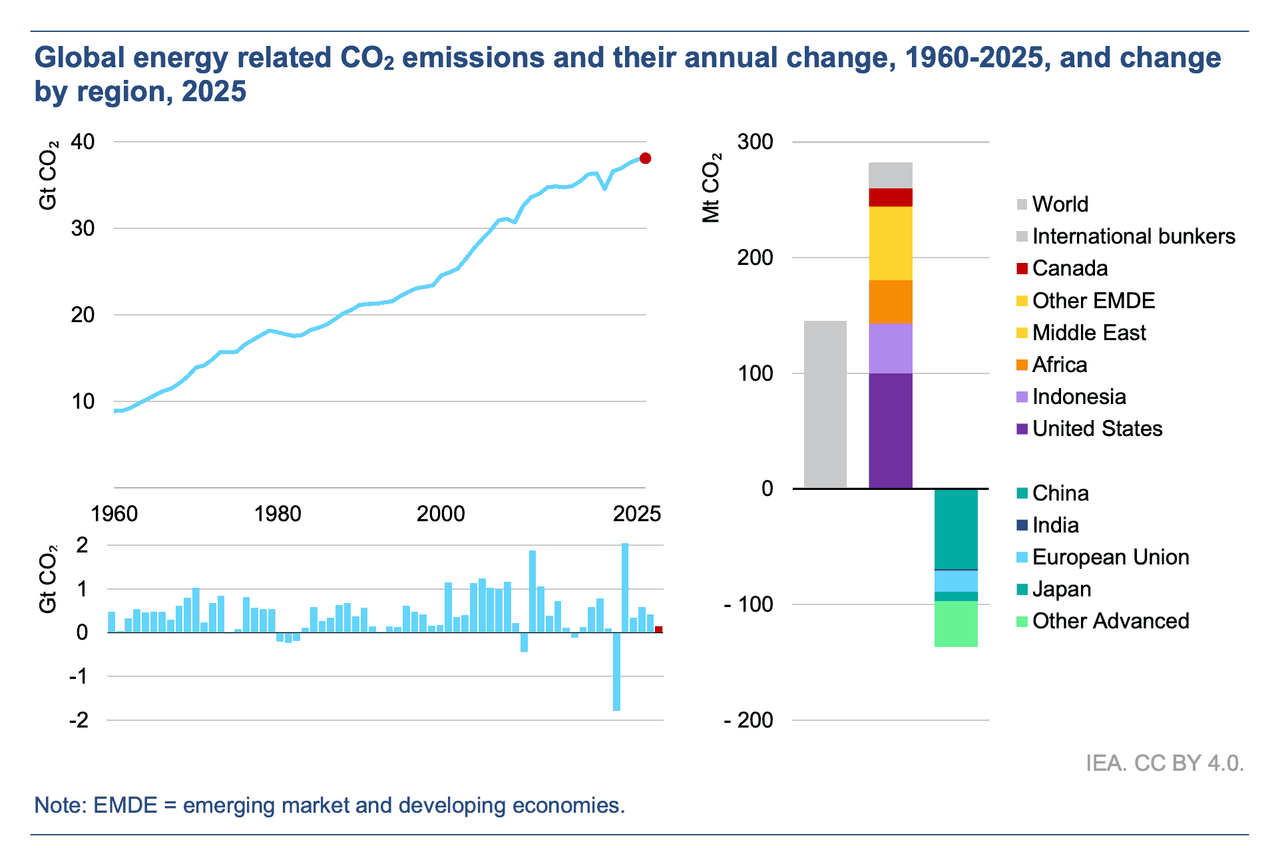

Energy sector emissions continued to rise in 2025, but regional trends varied markedly

Global growth in energy-related CO₂ emissions slowed in 2025, rising by around 0.4%, the slowest rate since 2021. Despite this slowdown, total energy-related CO₂ emissions increased by around 145 million tonnes (Mt) in 2025, reaching a new high of nearly 38.4 billion tonnes (Gt) ² , and 5% above 2019 levels. The increase coincided with record atmospheric CO₂ concentrations of about 427 parts-per-million (ppm), roughly 2.4 ppm higher than in 2024 and around 50% above pre-industrial levels.

Emissions from fuel combustion grew by close to 0.5% (around 185 Mt CO₂ ), while emissions from industrial processes declined by roughly 2% (about 40 Mt CO₂ ), partially offsetting the overall increase. Emissions growth remained below the pace of global economic expansion (global GDP increased by about 3.1% in 2025), indicating a continued decoupling between emissions and economic activity following the disruption observed earlier in the decade.

For the first time since the 1990s, advanced economies saw higher emissions growth than emerging economies

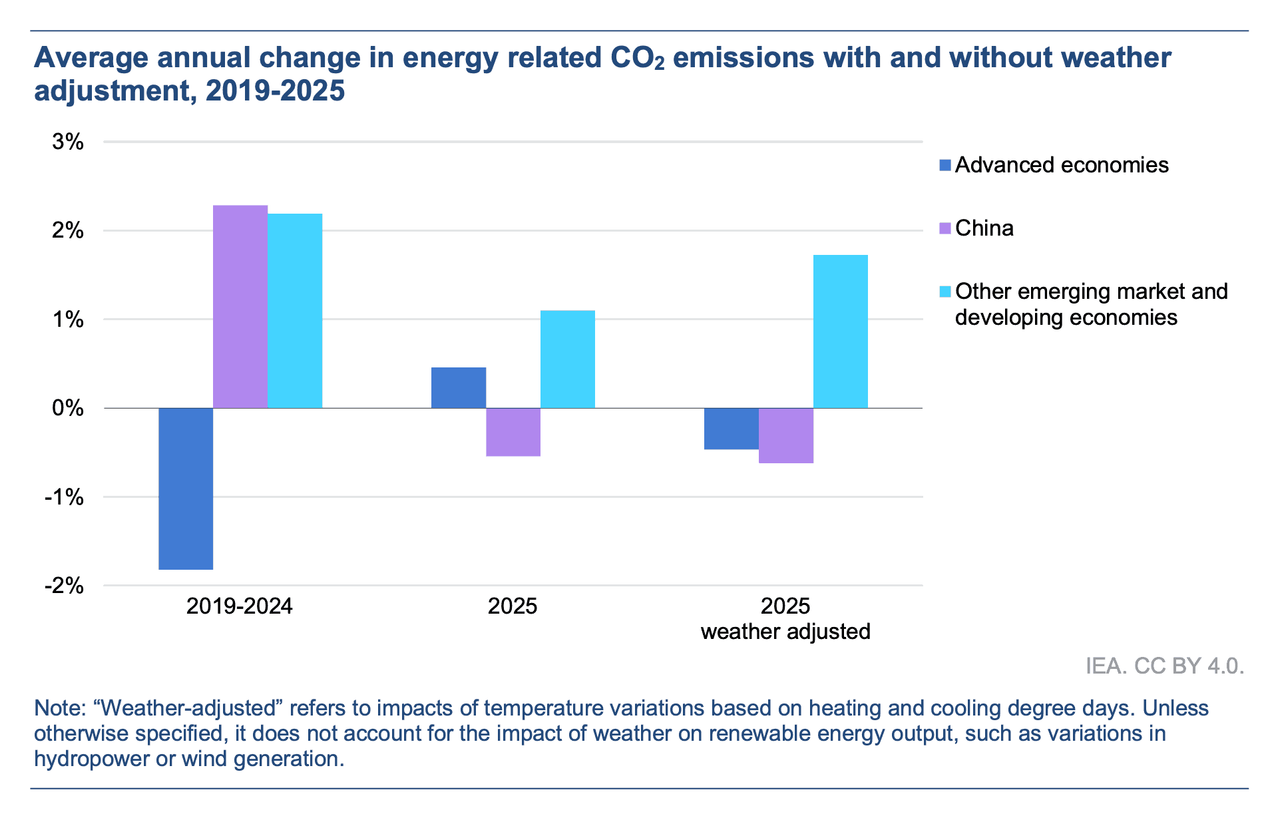

In 2025, global energy-related CO₂ emissions rose more strongly in advanced economies than in emerging market and developing economies for the first time in nearly 30 years. Emissions in advanced economies increased by 0.5%, while in emerging market and developing economies, growth slowed to 0.3%.

Emissions in China declined by around 0.5%, reflecting continued reductions in emissions from both industrial processes and electricity generation. This was mainly driven by a surge in low-emissions generation combined with slower electricity demand growth compared with 2024, and a notable contraction in cement and steel production. However, these effects were partially offset by the chemical industry. In emerging market and developing economies excluding China, emissions increased by 1.1%, significantly below the 2.2% average annual growth observed over the past five years, with India a major contributor to this slowdown. Emissions in India dipped in 2025, driven primarily by weather effects linked to an earlier and stronger monsoon cycle, alongside continued robust expansion of renewable energy capacity.

Outside of China, annual emissions trends were largely driven by weather effects. In advanced economies, colder winter conditions boosted heating demand, increasing natural gas consumption in buildings and the power sector. By contrast, reduced cooling needs in many emerging markets and developing economies moderated coal and electricity demand growth. On a weather-adjusted basis, CO₂ emissions in advanced economies would have declined by around 0.5%, reflecting continued structural improvements in energy efficiency and clean energy deployment. In emerging markets and developing economies outside of China, emissions would have increased by around 1.7% as weather played a substantial role in curbing emissions growth, notably in India and Southeast Asia.

Natural gas drove CO₂ emissions growth while coal emissions plateaued

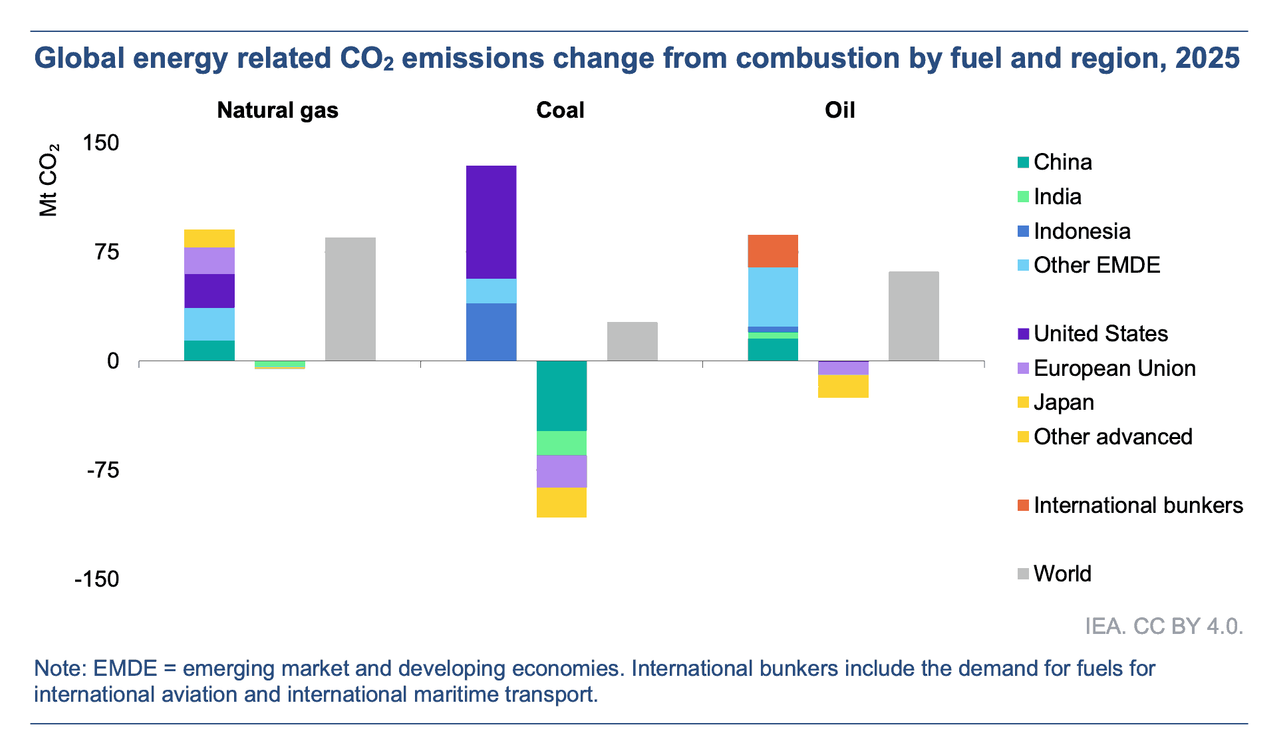

Natural gas was the largest contributor to the increase in global energy-related CO₂ emissions in 2025. Of the total 185 Mt CO₂ rise in emissions from fuel combustion, natural gas accounted for nearly half, or 85 Mt CO₂ , followed by oil at 60 Mt. Coal emissions plateaued, increasing by 25 Mt CO₂ (compared to 210 Mt CO₂ in the previous year), masking divergent regional trends. Higher natural gas prices supported gas-to-coal switching in the United States, adding more than 75 Mt, while China’s coal emissions fell, reflecting the country’s 1.4% decline in coal power generation. The increase in oil-related emissions was concentrated in China, India and other emerging market and developing economies, where rising transport activity and economic growth continued to support higher oil demand.

Weather effects also played a significant role in shaping fuel-specific trends in 2025. More than 40% of the growth in global natural gas demand was linked to higher heating needs in advanced economies, where colder winter conditions boosted consumption in buildings and the power sector. In India, lower coal use reflected reduced cooling demand due to milder temperatures and an earlier monsoon season. We estimate that weather effects decreased coal demand by around 8 million tonnes of coal equivalent (Mtce) in the country, reducing CO₂ emissions by over 20 Mt.

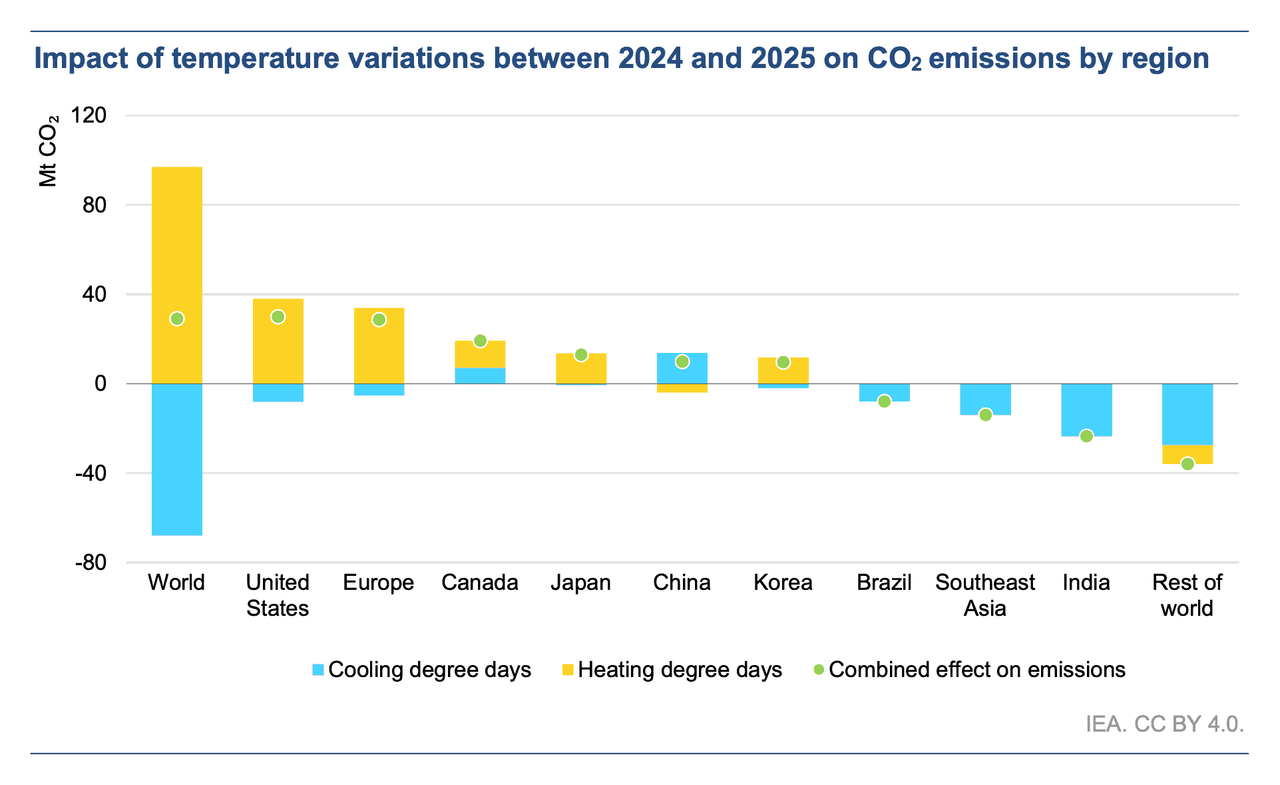

Temperature swings and drought conditions pushed up emissions

Global energy demand was shaped by continued temperature volatility in 2025, which was the third warmest year on record – slightly cooler than the record set in 2024. An earlier and more widespread monsoon season brought increased rainfall and cloud cover in India and Southeast Asia, reducing extreme heat and lowering air conditioning use. Without these milder conditions, the coal demand increase would have been around 30% higher globally. Despite this easing, cooling degree days remained well above the long-term average between 2000 and 2019, sustaining elevated electricity needs in many regions. At the same time, colder winters in advanced economies increased heating degree days and shifted energy consumption toward heating fuels compared with 2024.

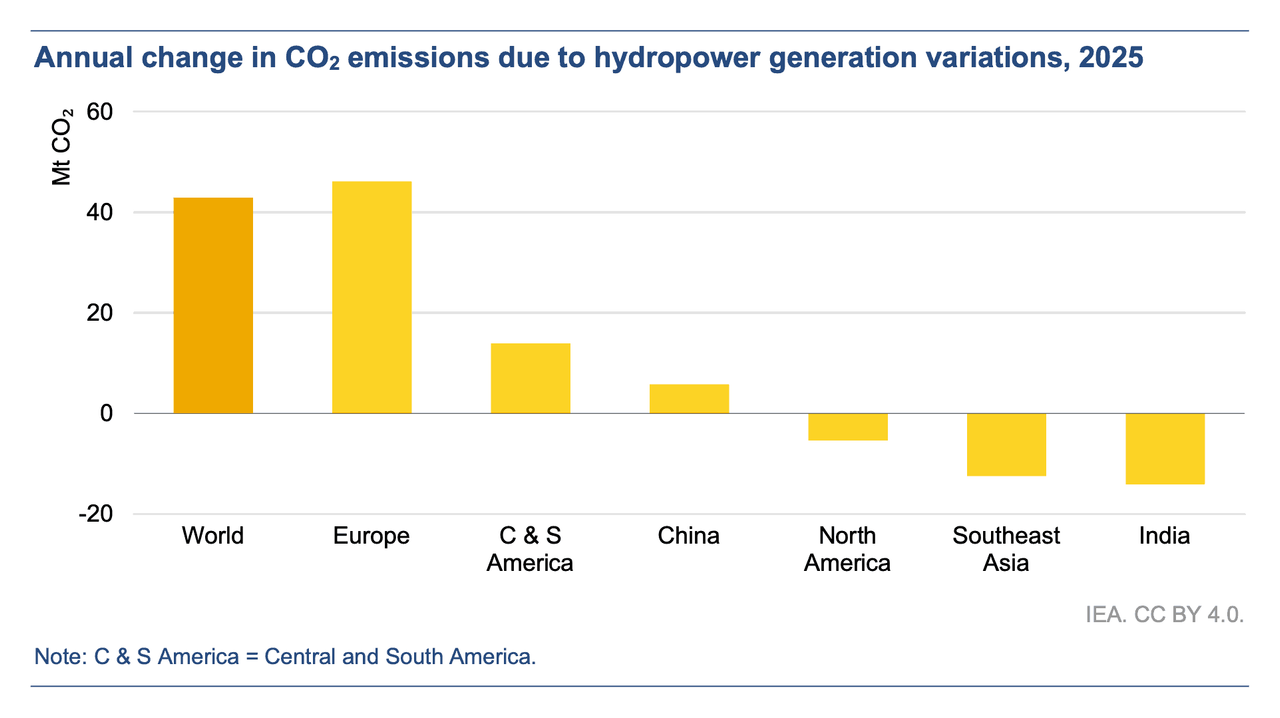

Beyond temperature effects, drought conditions in several regions, particularly in Europe and across Central and South America, constrained hydropower output. The resulting shortfall was largely met by higher fossil fuel output, leading to an estimated additional 40 Mt of CO₂ emissions globally.

Europe was largely drier than normal, and hot summer temperatures exacerbated drought conditions, particularly in western and eastern portions of the continent. Had the availability of the hydropower fleet in 2025 remained consistent with 2024 levels, an additional 75 TWh of electricity would have been generated in the region, avoiding around 45 Mt of CO₂ from fossil fuel-based power plants. Weaker average daily wind speeds also reduced wind power output compared to 2024, increasing reliance on fossil-fuel based generation. If wind conditions had been the same as 2024, over 20 Mt CO₂ would have been avoided in Europe.

Excluding winter precipitation, India recorded above-normal rainfall across all seasons, with May precipitation reaching its highest level since 1901. This early onset of the southwest monsoon boosted hydropower output and contributed to an estimated reduction in emissions of around 15 Mt CO₂.

We estimate that the net impact of weather-related factors – including temperature variations and shortfalls in hydropower and wind – pushed up CO₂ emissions from the combustion of fossil fuels by around 90 million tonnes in 2025, accounting for around half of the total 185 Mt rise in combustion emissions.

————————————

² This includes CO₂ emissions from fuel combustion, industrial processes, and fugitive (flaring). Elsewhere in this report, unless explicitly mentioned, CO₂ emissions refer to emissions from fuel combustion and industrial processes excluding fugitive (flaring).

Global growth in energy-related CO₂ emissions slowed in 2025, rising by around 0.4%, the slowest rate since 2021. Despite this slowdown, total energy-related CO₂ emissions increased by around 145 million tonnes (Mt) in 2025, reaching a new high of nearly 38.4 billion tonnes (Gt) ² , and 5% above 2019 levels. The increase coincided with record atmospheric CO₂ concentrations of about 427 parts-per-million (ppm), roughly 2.4 ppm higher than in 2024 and around 50% above pre-industrial levels.

Emissions from fuel combustion grew by close to 0.5% (around 185 Mt CO₂ ), while emissions from industrial processes declined by roughly 2% (about 40 Mt CO₂ ), partially offsetting the overall increase. Emissions growth remained below the pace of global economic expansion (global GDP increased by about 3.1% in 2025), indicating a continued decoupling between emissions and economic activity following the disruption observed earlier in the decade.

For the first time since the 1990s, advanced economies saw higher emissions growth than emerging economies

In 2025, global energy-related CO₂ emissions rose more strongly in advanced economies than in emerging market and developing economies for the first time in nearly 30 years. Emissions in advanced economies increased by 0.5%, while in emerging market and developing economies, growth slowed to 0.3%.

Emissions in China declined by around 0.5%, reflecting continued reductions in emissions from both industrial processes and electricity generation. This was mainly driven by a surge in low-emissions generation combined with slower electricity demand growth compared with 2024, and a notable contraction in cement and steel production. However, these effects were partially offset by the chemical industry. In emerging market and developing economies excluding China, emissions increased by 1.1%, significantly below the 2.2% average annual growth observed over the past five years, with India a major contributor to this slowdown. Emissions in India dipped in 2025, driven primarily by weather effects linked to an earlier and stronger monsoon cycle, alongside continued robust expansion of renewable energy capacity.

Outside of China, annual emissions trends were largely driven by weather effects. In advanced economies, colder winter conditions boosted heating demand, increasing natural gas consumption in buildings and the power sector. By contrast, reduced cooling needs in many emerging markets and developing economies moderated coal and electricity demand growth. On a weather-adjusted basis, CO₂ emissions in advanced economies would have declined by around 0.5%, reflecting continued structural improvements in energy efficiency and clean energy deployment. In emerging markets and developing economies outside of China, emissions would have increased by around 1.7% as weather played a substantial role in curbing emissions growth, notably in India and Southeast Asia.

Natural gas drove CO₂ emissions growth while coal emissions plateaued

Natural gas was the largest contributor to the increase in global energy-related CO₂ emissions in 2025. Of the total 185 Mt CO₂ rise in emissions from fuel combustion, natural gas accounted for nearly half, or 85 Mt CO₂ , followed by oil at 60 Mt. Coal emissions plateaued, increasing by 25 Mt CO₂ (compared to 210 Mt CO₂ in the previous year), masking divergent regional trends. Higher natural gas prices supported gas-to-coal switching in the United States, adding more than 75 Mt, while China’s coal emissions fell, reflecting the country’s 1.4% decline in coal power generation. The increase in oil-related emissions was concentrated in China, India and other emerging market and developing economies, where rising transport activity and economic growth continued to support higher oil demand.

Weather effects also played a significant role in shaping fuel-specific trends in 2025. More than 40% of the growth in global natural gas demand was linked to higher heating needs in advanced economies, where colder winter conditions boosted consumption in buildings and the power sector. In India, lower coal use reflected reduced cooling demand due to milder temperatures and an earlier monsoon season. We estimate that weather effects decreased coal demand by around 8 million tonnes of coal equivalent (Mtce) in the country, reducing CO₂ emissions by over 20 Mt.

Temperature swings and drought conditions pushed up emissions

Global energy demand was shaped by continued temperature volatility in 2025, which was the third warmest year on record – slightly cooler than the record set in 2024. An earlier and more widespread monsoon season brought increased rainfall and cloud cover in India and Southeast Asia, reducing extreme heat and lowering air conditioning use. Without these milder conditions, the coal demand increase would have been around 30% higher globally. Despite this easing, cooling degree days remained well above the long-term average between 2000 and 2019, sustaining elevated electricity needs in many regions. At the same time, colder winters in advanced economies increased heating degree days and shifted energy consumption toward heating fuels compared with 2024.

Beyond temperature effects, drought conditions in several regions, particularly in Europe and across Central and South America, constrained hydropower output. The resulting shortfall was largely met by higher fossil fuel output, leading to an estimated additional 40 Mt of CO₂ emissions globally.

Europe was largely drier than normal, and hot summer temperatures exacerbated drought conditions, particularly in western and eastern portions of the continent. Had the availability of the hydropower fleet in 2025 remained consistent with 2024 levels, an additional 75 TWh of electricity would have been generated in the region, avoiding around 45 Mt of CO₂ from fossil fuel-based power plants. Weaker average daily wind speeds also reduced wind power output compared to 2024, increasing reliance on fossil-fuel based generation. If wind conditions had been the same as 2024, over 20 Mt CO₂ would have been avoided in Europe.

Excluding winter precipitation, India recorded above-normal rainfall across all seasons, with May precipitation reaching its highest level since 1901. This early onset of the southwest monsoon boosted hydropower output and contributed to an estimated reduction in emissions of around 15 Mt CO₂.

We estimate that the net impact of weather-related factors – including temperature variations and shortfalls in hydropower and wind – pushed up CO₂ emissions from the combustion of fossil fuels by around 90 million tonnes in 2025, accounting for around half of the total 185 Mt rise in combustion emissions.

————————————

² This includes CO₂ emissions from fuel combustion, industrial processes, and fugitive (flaring). Elsewhere in this report, unless explicitly mentioned, CO₂ emissions refer to emissions from fuel combustion and industrial processes excluding fugitive (flaring).

IEA (2026), Global Energy Review 2026, IEA, Paris https://www.iea.org/reports/global-energy-review-2026, Licence: CC BY 4.0